Hungary

Hungary

- Water Snapshot

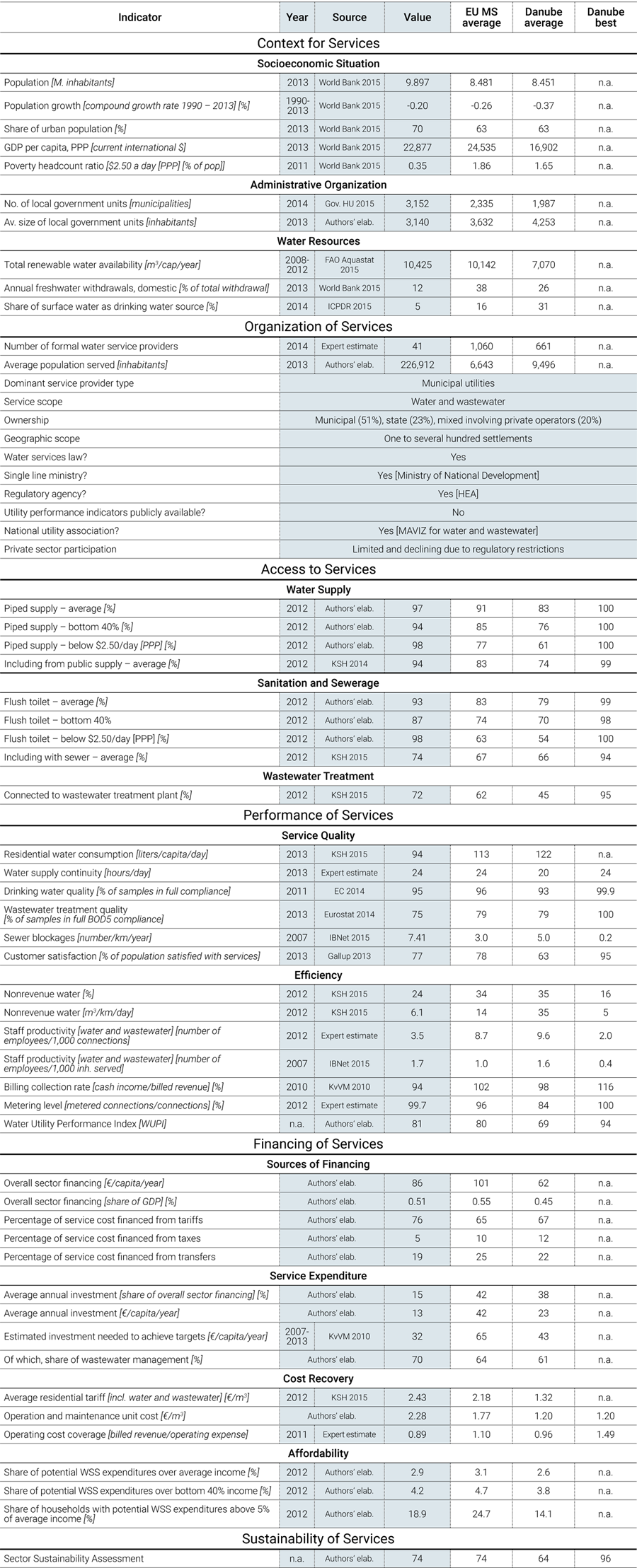

- Context for Services

- Organization for Services

- Access to Services

- Performance of Services

- Financing of Services

- Water Sector Sustainability and Main Challenges

- Sources

WATER SNAPSHOT

Sources for all numbers in the snapshot are provided in full in the body of this country page; a complete description of the methodology is provided in the State of the Sector Regional Report available under SoS.danubis.org/Report.

|

|

KEY WATER AND SANITATION SECTOR CHALLENGES

- Achieving full cost recovery. Many of Hungary’s water utilities have carried out EU and government-sponsored investments in the last few years. As a result of the financing agreement, the depreciation of these investments must be covered by tariffs. But the future maintenance costs of these recent development projects still have to be included in the price of the services. Moreover, since water and sewerage tariffs were frozen in 2012 and were decreased by law in 2013, revenues collected by utilities are decreasing.

- Preventing the degradation of assets in the longterm. While assets of most water utilities have been properly maintaining their assets for the last two decades, few companies have made an effort to create sufficient reserves for their future replacement. As a result, the infrastructure is aging and its average condition is slowly declining. Due to the 2013 tariff cut, utilities have accumulated even lower reserves than before, and maintenance has become problematic for many operators.

- Preparing for the risks caused by climate change. Most water utility managers are aware of the types of risks caused by climate change (such as new patterns of precipitation, stress on sewers, changing patterns of water consumption, and change in water resources used for drinking water), but the everyday challenges of maintaining a high level of operation under worsening financial conditions make it difficult to focus on the long term, and there has been almost no preparation to address the identified risks of climate change.

FURTHER RESOURCES

On water services in the Danube Region

- A regional report analyzing the State of Sector in the region, as well as detailed country notes for15 additional countries, are available under SoS.danubis.org

- Detailed utility performance data is accessible, if available, under www.danubis.org/database

On water services in Hungary

The following documents are recommended for further reading; the documents, and more, are available at www.danubis.org/eng/country-resources/hungary/

- KvVM. 2010. National River Basin Management Plan. Budapest: Hungarian Ministry of Environment and Water.

- MinRD. 2013. Water Strategy. Budapest: Hungarian Ministry of Rural Development.

- Tamás, H.M. and P. Gábor. 2012. Nem folyik az többé vissza: Az állam szerepének átalakulása a víziközmű-szolgáltatásban. Budapest: Hungarian Academy of Sciences.

CONTEXT FOR SERVICES

Economy. Hungary is an upper-middle-income country with substantial regional differences. GDP per capita is higher in Central Hungary, which includes Budapest, where this indicator is slightly above the EU average. In Western Hungary, the GDP per capita falls between 75% and 100% of the EU average, while for the rest of the country (South, North, and Eastern Hungary), this value is between 50% and 75% of the EU average. Various other indicators (e.g., unemployment levels, investments, access to highways, life expectancy) show a similar disparity. Hungary has been an EU Member State since May 2004 (GVI 2013).

Governance. The guiding principle of recent regulatory reforms has been centralization; i.e., increasing the role of the central government and reducing the responsibilities and resources of municipalities. Hungary is a unicameral parliamentary republic and the government directs and oversees the operation of the state administration. Hungary’s public administrative regional units are comprised of the capital city and 19 counties. Budapest is composed of 23 districts. There are 3,152 cities and municipalities in Hungary (Gov. HU 2015). Each county and district in Budapest is self-governed. The government is responsible for most water utility governance, but the municipalities and central government are responsible for water and sanitation service provision.

Water resources. Water resources in Hungary show regional and seasonal limitations, which may escalate with climate change. Hungary has sufficient water resources, but there are significant differences in regional distribution. The total renewable freshwater quantity is 10,425 m3/capita/year (FAO Aquastat 2015), and the overall quality is good, but two-thirds of the recent subsurface consumption is supplied from water bodies in weak or uncertain status. In response to climate change, a national climate strategy (NÉS) was adopted in 2008, and in 2013, a separate national water strategy was created that emphasizes the protection of water resources. These documents primarily address the necessary measures needed to cope with the consequences of parallel increases in drought and flood frequency on the economy and the environment. Urban heat waves are a specified vulnerability for Hungary that could have a direct connection to water utilities. Better management of precipitation and the creation of storage facilities to meet nondrinking water needs are envisaged to reduce this vulnerability. Flood protection actions target the reinforcement of dykes and the creation of flood water storage reservoirs to lower peak flood levels. The use of subsurface resources cushions the sector from the most direct effects of climate change.

Water supply sources. Bank-filtered and subsurface resources are the key source of water supply. The direct use of surface water for domestic/public purposes is minor (5%), whereas bank-filtered resources (indirect service provided from surface water) represent 40.5%. The domestic/public consumption of subsurface resources amounts to 54.5% of the overall water resources used (KvVM 2010). The bank-filtered resources are generally of good quality and quantity. However, they are dependent on river morphology developments. The use of subsurface water resources is concentrated, and there are local resource constraints with respect to the volume of extraction. Shallow subsurface sources are often polluted, especially from agricultural sources.

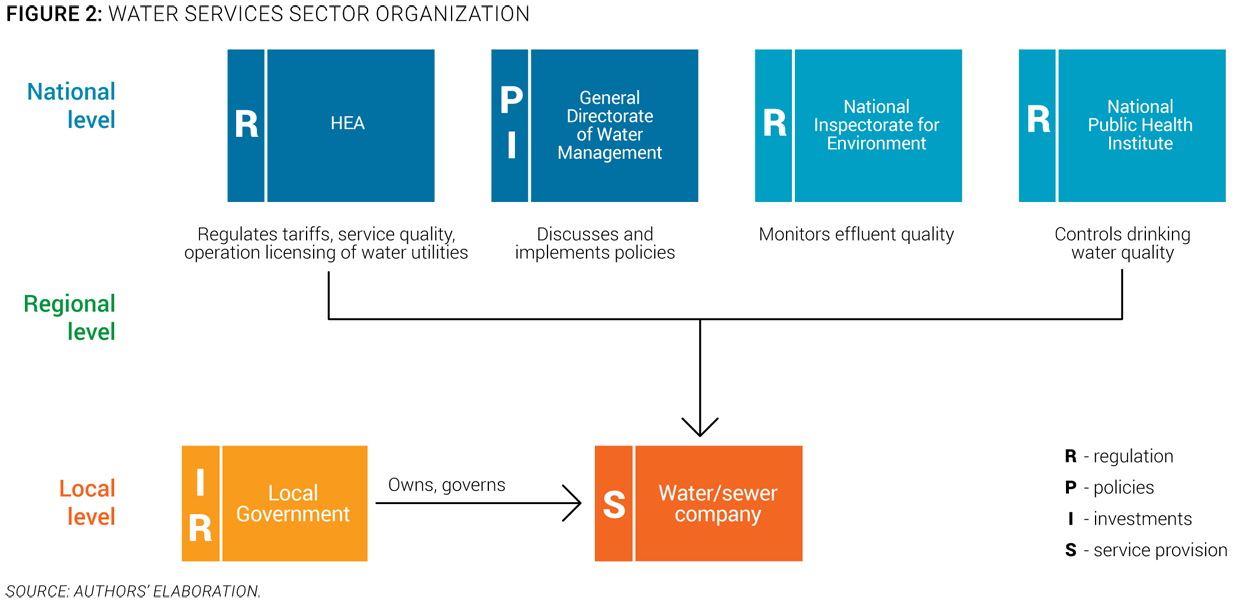

ORGANIZATION FOR SERVICES

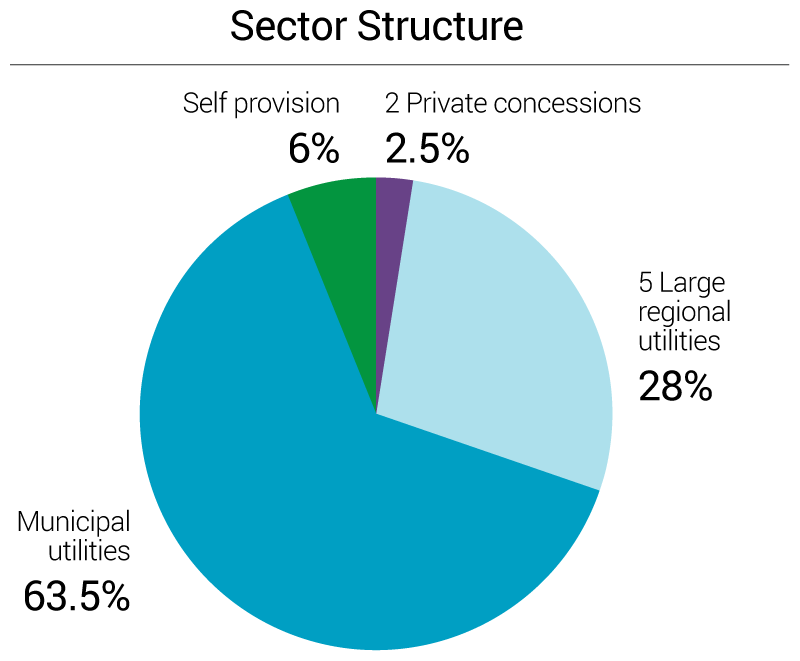

Service provision. Municipalities and the central government are responsible for service provision. Depending on the ownership of assets, there is a mixed responsibility for service provision between the central government and municipalities. Before 2012, there were close to 400 water utilities. As a result of a water utility sector reform, this number decreased to 41 in 2015 (Figure 1). By 2017, the minimum required size to obtain a license for operation will be 150,000 population equivalent (p.e.). Almost all municipal utilities serve several towns and villages, some of them covering over 100 settlements. The assets of these companies and of the service provider utility company are owned by the participating municipalities. The five regional utilities are predominantly state owned (only a few percent of shares are owned by municipalities and employees), while the assets used for service provision are partly state owned and partly municipally owned. Each of these companies serves over 100 settlements. There are two water and wastewater concessions serving 2.5% of the population, located in Szeged (Szegedi Vízmű) and Szolnok (Víz és Csatornaművek Koncessziós ZRt). There is also one wastewater only concession in Budapest (FCSM). State or municipal water utilities serve 91.5% of the inhabitants. The rest of the population relies on self-provision (6%).

Policy-making and sector institutions. Since 2012, the Hungarian Energy and Public Utility Regulatory Authority (HEA) has been the key institution that regulates and oversees the water sector. The 2011 sector reform in its Act CCIX on Water Utility Supply established a central regulator, replacing a primarily municipally regulated system. There is also a clear line ministry and no overlapping between mandates of the institutions involved in the sector. At the national level, the key stakeholders are (Figure 2):

- The Hungarian Energy and Public Utility Regulatory Authority (HEA), which is responsible for economic regulation, licensing, and monitoring of the water and sanitation sector.

- The Ministry of National Development, which is responsible for approving the tariffs proposed by HEA.

- The General Directorate of Water Management, which is part of the Ministry of the Interior, which is the line ministry for the water sector. Its regional bodies are responsible for management of the state-owned infrastructure against water damage, and for water management.

- The National Public Health and Medical Officer Service, which is responsible for monitoring drinking-water quality, through its county-level bodies.

- The National Inspectorate for Environment, Nature and Water, which is part of the Ministry of Agriculture and which is in charge of monitoring effluent discharges and the environmental status of water bodies. It also issues water extraction and wastewater discharge licenses.

Capacity and training. There is no formal training institute for the water utility sector. The water utility association (MAVIZ) organizes occasional training sessions, workshops, and conferences. Staff are usually highly qualified, especially in large water utilities, and staff turnover is generally not a problem.

Economic regulation. The central regulator, HEA, is in charge of developing tariff proposals for approval by the Minister of National Development. Based on the tariff-setting regulation (a government decree) currently under development, water utilities will submit detailed information to the water utility regulator, which will make a tariff proposal to the Minister of National Development, which will set the tariff. A new tariff methodology is under development. Two-part tariffs are prescribed by law, and up to 50% of cross-financing between commercial and household customers is allowed. Until the above-mentioned decree is passed, tariffs were frozen at current levels in 2012 and further decreased by law in 2013. They will probably be set according to the new regulation in 2016.

Ongoing or planned reforms. An ongoing water utility sector reform, which started in 2011 and is expected to be completed by 2016, seeks to establish a central agency responsible for the economic regulation of the sector. The former Hungarian Energy Office is enlarged (into a Public Utility Regulator, HEA), and regulatory tasks related to other sectors are included in the regulatory scope of HEA. Water utilities can operate only if they have a license issued by HEA, which underscores the power of the regulator in licensing. The regulation prescribes a minimum utility size, measured as population equivalent being served. The lowest accepted value of this figure is 150,000 p.e. Water utilities therefore must reach this size by 2016, with some intermediate deadlines to show progress. The number of utilities has already fallen from around 400 to under 50. Water utilities are obliged to make rolling investment plans for a period of 15 years and submit them for approval by the HEA each year. Private participation is seriously restricted for both investments by private partners and outsourcing.

Regionalization

Act CCIX on Water Utilities declared that the integration of water utilities is a goal of principle, setting a minimum size requirement of 150,000 population equivalent (p.e.) to be reached by December 31, 2016. To promote the timely execution of mergers, the regulation also declared a transitional deadline of 100,000 p.e. by December 31, 2014. Among others, meeting the prescribed size is a precondition to obtaining an operating license from HEA. Given the minimum size requirement, utilities and municipalities had an incentive to start negotiations in order to complete mergers or establish new operating contracts. As a result, regionalization was a “free will” process among sector players.

When a small municipal water utility is not able to get an operating license, and the municipality is unable to contract with a larger licensed utility, HEA is entitled to designate an existing large utility as the “operator of last resort,” which then has to provide services to the municipality for a temporary period. Today, there are 41 water utilities in Hungary, and this number is expected to further decline by the end of 2016. The five state-owned regional utilities had a major role in integrating the smallest service providers, fulfilling their informally acquired mission.

ACCESS TO SERVICES

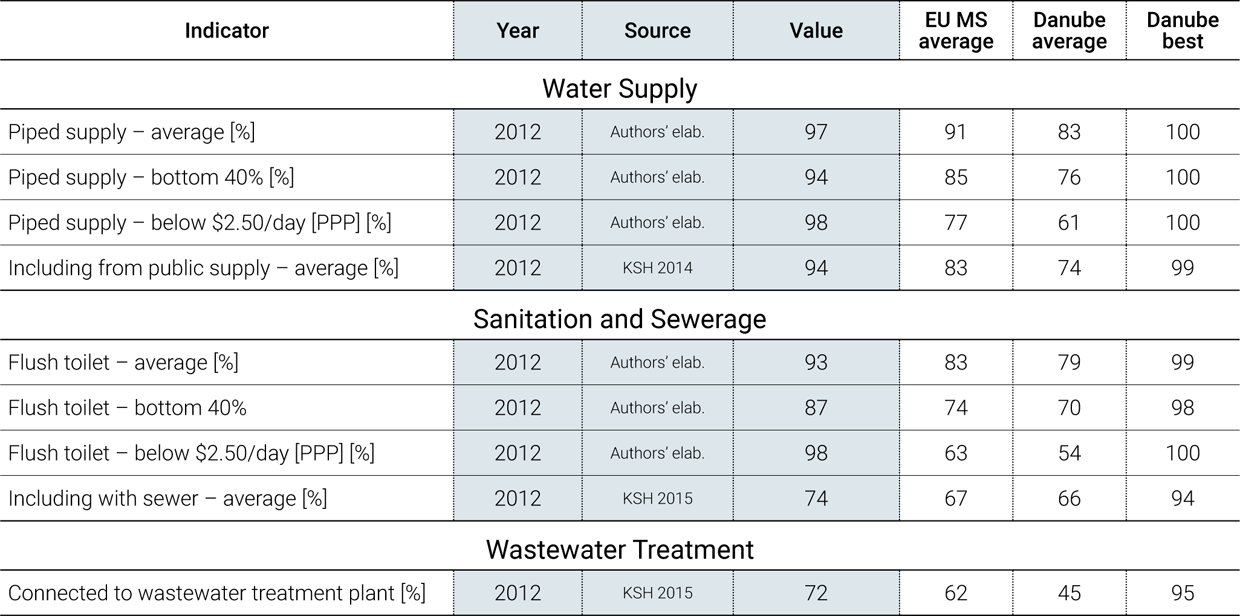

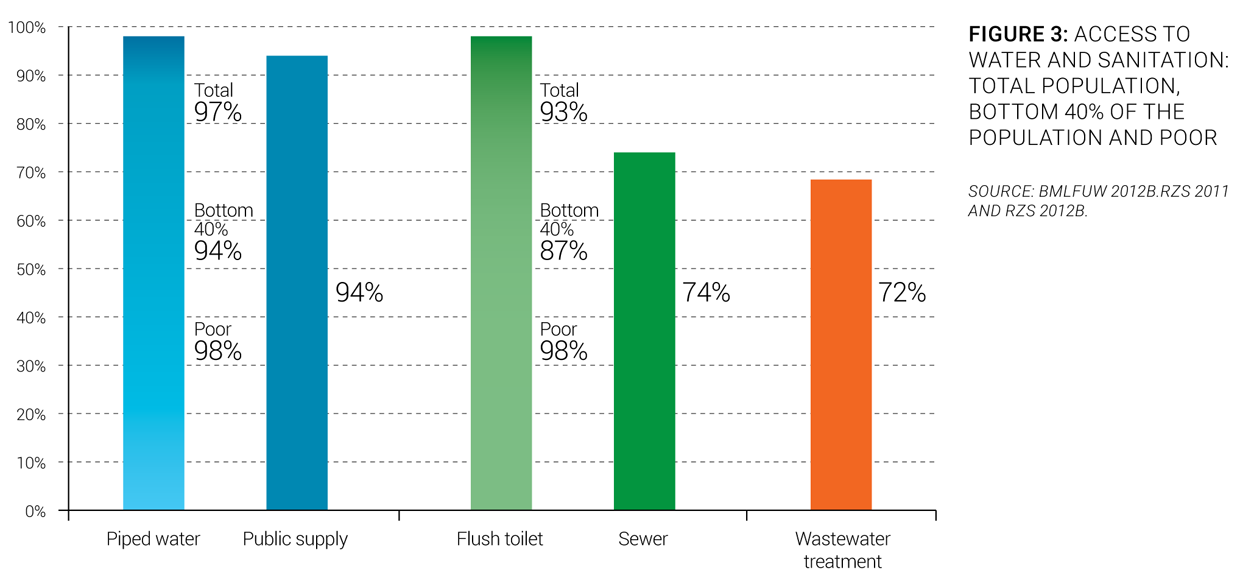

Service coverage. Hungarian utilities provide almost full access to drinking water services, and there is a declining gap between water and sewer connections. Ninety-seven percent of the population is connected to drinking water networks (Authors’ elaboration). The connection rate to the sewer system increased from 46% in 1990 to 74% in 2012 (Figure 3), with urban connection rates of 85% and rural rates of 47% (KSH 2015). Almost three-quarters of collected wastewater is treated at least at the secondary level (KSH 2015).

Equity of access to services. Low-income households and vulnerable ethnic minorities have below-average access to services. Ninety percent of the lowest quintile of households and 94% of the bottom 40% have access to piped drinking water, compared to the national average of 97%. Access to flush toilets is 87% for the bottom 40% (Authors’ elaboration). The majority of the Roma minorities are in the lowest quintile.

Service infrastructure. The water network is mature, while some upgrading is still needed for sanitation infrastructure. The drinking water network is complete, while wastewater network coverage stands at 74% (KSH 2015), and still growing, although at a slower pace during the last few years. Sewers on average are younger than water mains. The condition of drinking water treatment plants ranges from average to good, but in some municipalities additional treatment (especially arsenic removal) is needed, for which investment projects are underway. The sewage from all medium and large towns is treated to at least secondary level. Wastewater management of many small (below 2,000 p.e.) settlements still needs to be addressed.

PERFORMANCE OF SERVICES

Service Quality

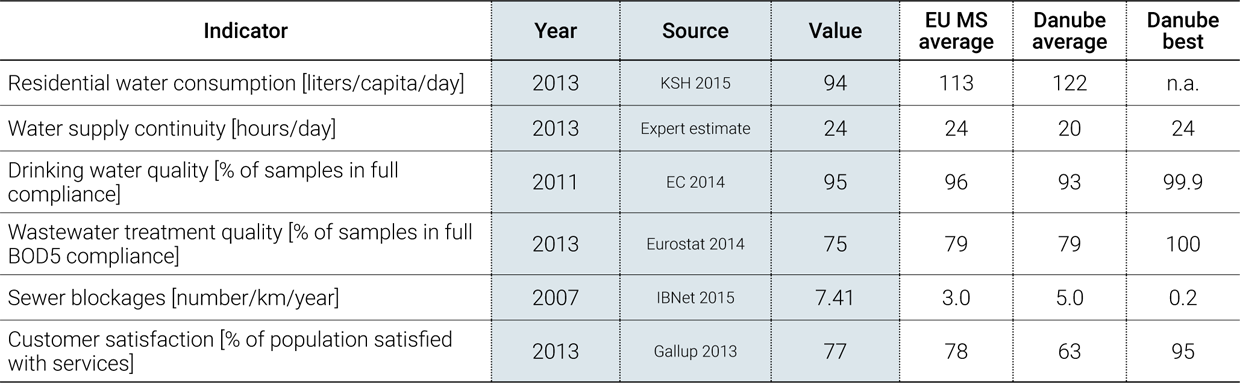

Quality of service. Water utility services standards are high. Water service is provided 24/7 (Expert estimate) and drinking water quality compliance is estimated to reach 95% (EC 2014). Where drinking water quality is problematic, alternative and temporary solutions are provided by water services (e.g., distribution of bottled water). Due to the overwhelming share of subsurface resources, however, several mineral elements exceed the mandatory thresholds. As a result, 40% of the settlements representing 25% of the population from time to time consume drinking water with mineral parameters above the standards. These minerals are arsenic, nitrogen compounds, iron, and manganese (KvVM 2010). Quality improvement programs are in progress, and an official update on the status of drinking water quality will be available after completion of the second round of the National Water Basin Management Plan, due in 2015.

Customer satisfaction. Most customers are satisfied with water services and water quality. While there are no nationwide domestic surveys on this topic, customers are primarily satisfied with service levels and drinking water quality. Seventy-seven percent of Hungarian citizens responding to the international Gallup survey responded that they were satisfied with the quality of drinking water, placing Hungary in the top countries surveyed (Gallup 2013).

Exporting know-how

The largest Hungarian drinking water service provider, the Budapest Waterworks, makes use of its wide-ranging knowledge and experience, including through international partnerships. The company has projects in, for example, Azerbaijan, Russia, Sri Lanka, and Vietnam, in the field of project design and execution, modernization of assets, IT solutions, and the corresponding training of local staff. Project organization, subcontracting, and setting up joint ventures are all viable forms of cooperation.

Efficiency of Services

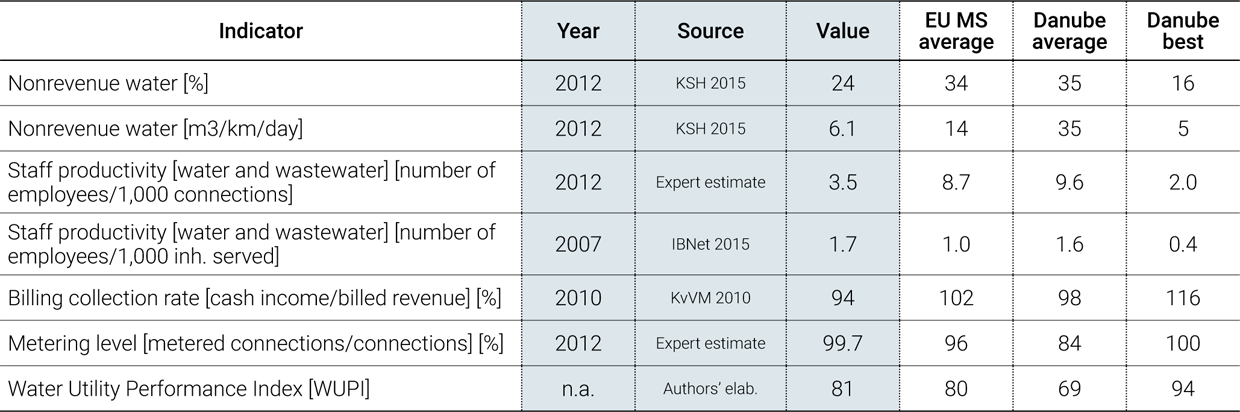

Overall efficiency. The overall efficiency of the sector is good, with significant variations across utilities. For most performance indicators, the water sector in Hungary displays above average performance in a regional comparison. Nevertheless, behind these average figures, there are notable variations of efficiency among utilities. Nonrevenue water reached 24% in 2012, or 6.1 m3/km/day (KSH 2015). This level shows good technical operational performance of services compared to other countries in the Danube region. However, nonrevenue water varies from 10% to 45% among Hungarian water utilities (KSH 2015). The collection ratio is estimated at 94%, which indicates that utilities are able to collect invoices from customers, thus generating revenues (KvVM 2010). Moreover, the average number of staff per 1,000 connections is low at 3.5 (Expert estimate). This is among the best practice observed in the countries of the Danube region, but it varies from 2 to 10 across the sector.

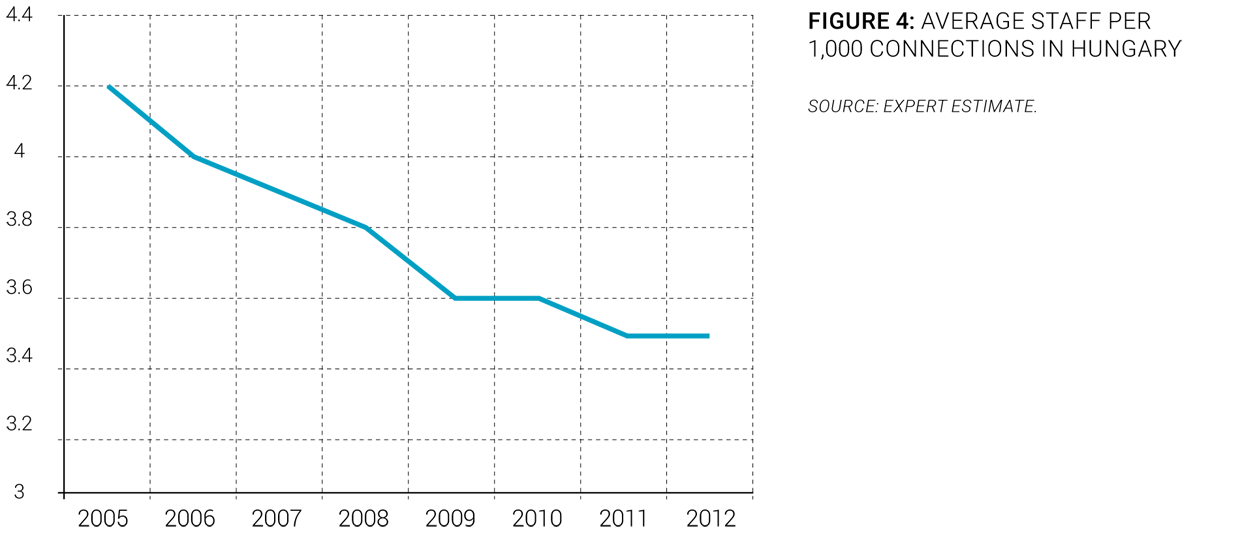

Recent trends. At present, there are no clear trends in efficiency changes. After major improvements during the 1990s and the beginning of the 2000s, the performance of water utilities in Hungary levelled off for the last 5 to 10 years. Nonrevenue water expressed in percent remained stable between 2001 and 2012, while nonrevenue water expressed in m3/km/day decreased by 9% over the same period (KSH 2015). The collection ratio also remained stable over the last 10 years, and no significant improvement has been noticed. The metering level has steadily increased since 2001 to nearly 100% today (Expert estimate), while water consumption per capita decreased by 6%, from 100 l/capita/day in 2001 to 94 l/capita/day in 2012 (KSH 2015). The number of staff per 1,000 connections has steadily and slowly decreased over the last decade (Figure 4), allowing a reduction in the operating costs of utilities. Small utilities are generally of lower efficiency than larger ones. After the ongoing mergers of the water utility reform process, the average efficiency figures are expected to further improve.

FINANCING OF SERVICES

Sector Financing

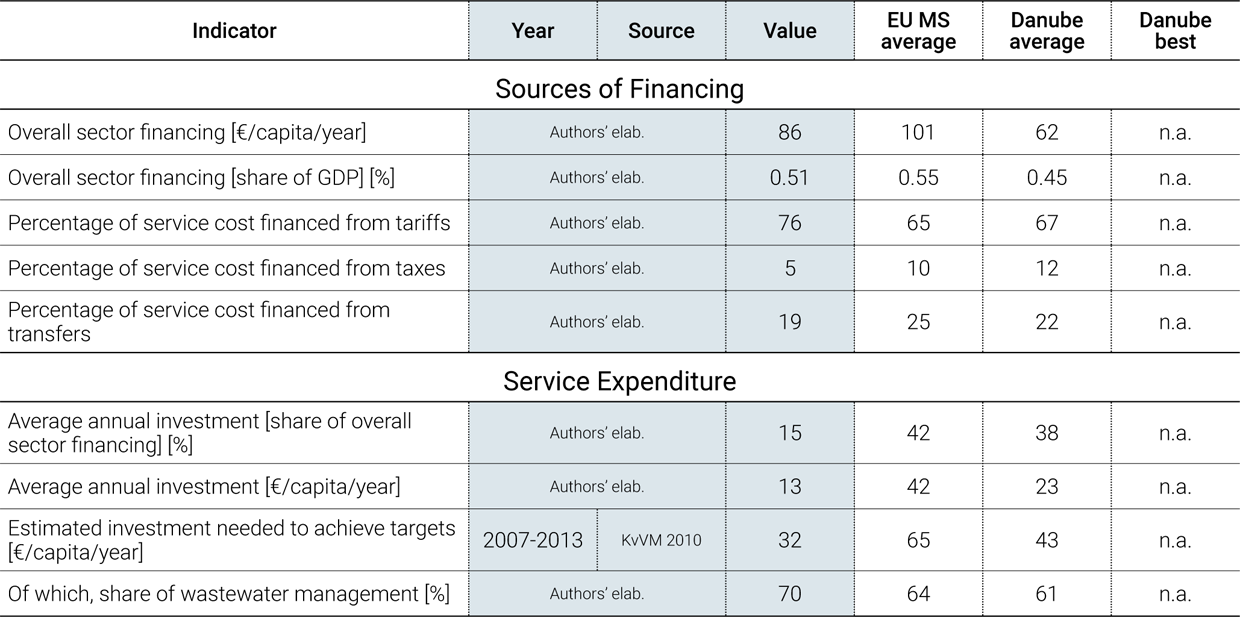

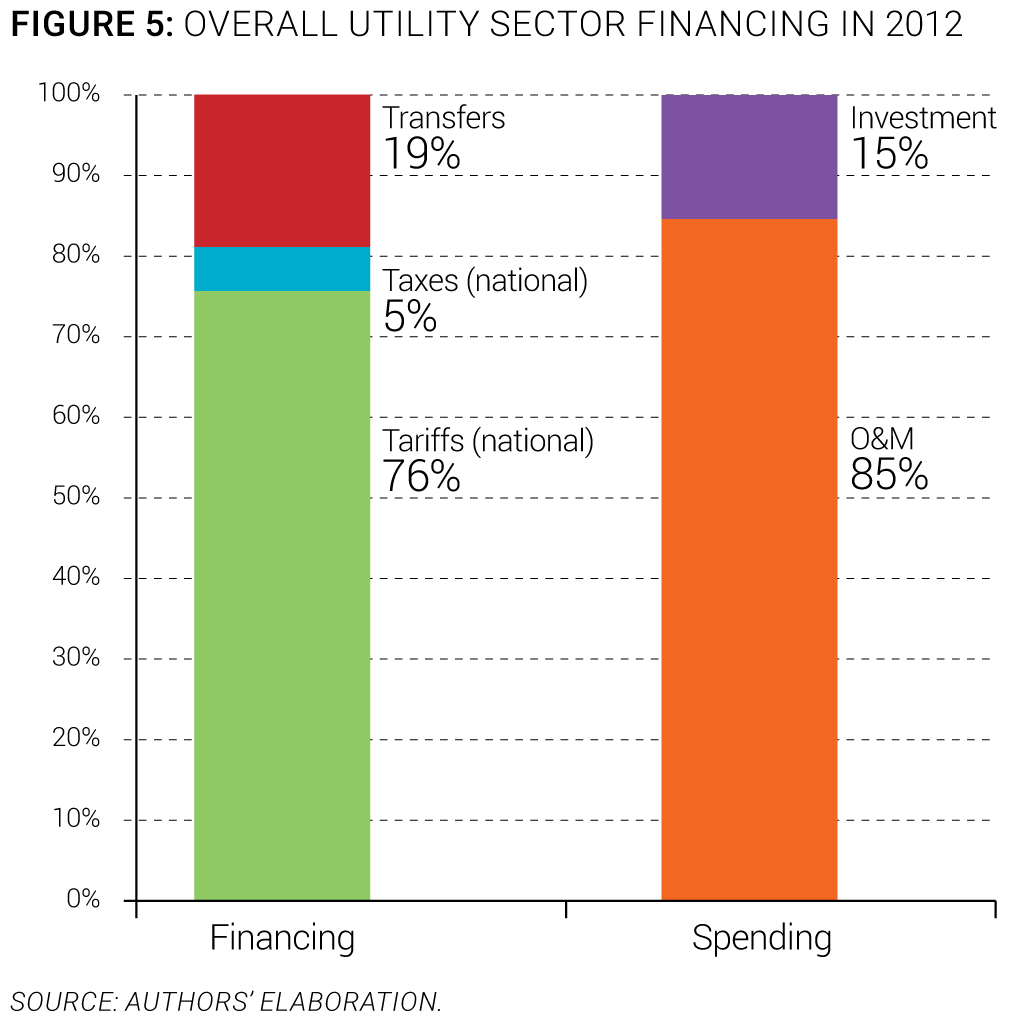

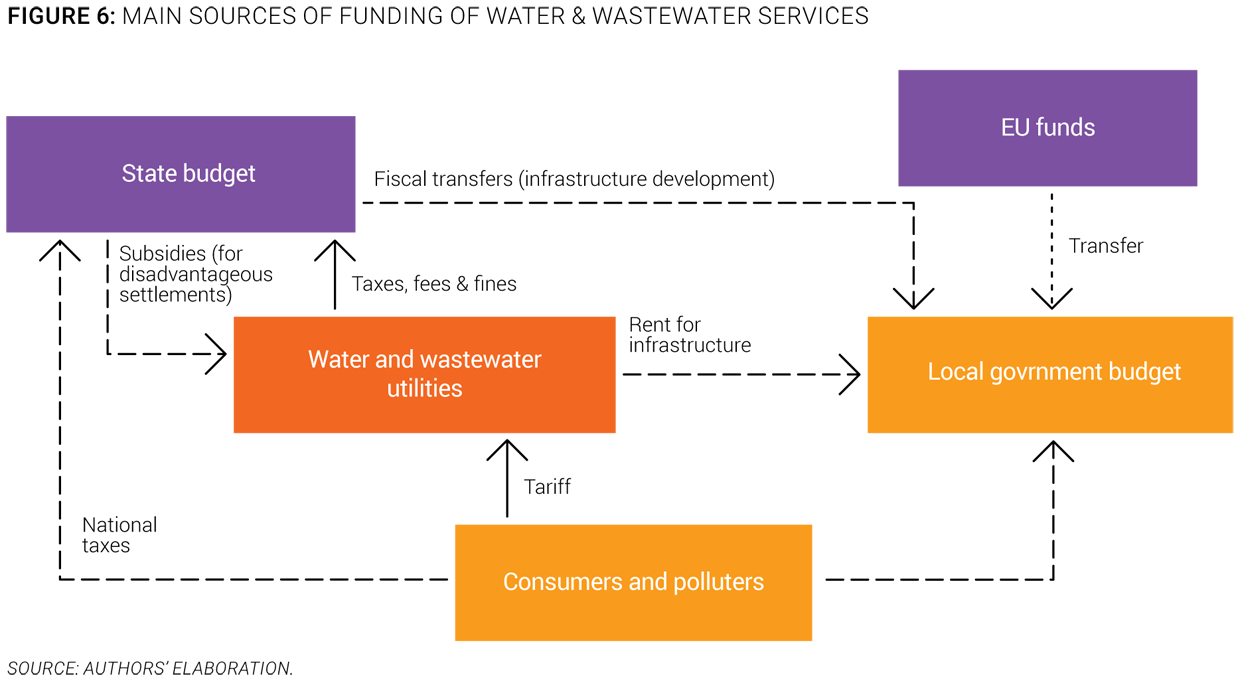

Overall sector financing. O&M costs are financed mainly through tariffs and new investments through external grants (Figure 5). Government subsidies are available to support the tariffs of municipalities where service costs are above a threshold level that is determined each year. Reconstruction work is usually financed through tariff revenues, but since water and sewerage tariffs were frozen and then decreased by law, funds to support reconstruction have been falling. New large-scale investments, such as network expansion, advanced drinking water treatment (especially to treat arsenic and other location-specific pollutants), and wastewater treatment plant construction and upgrades are financed mainly from EU and government funds.

The main sources of funding of water and wastewater utilities are described in Figure 6, using the OECD three Ts methodology (tariffs, transfers, and taxes).

Investment needs. Investment needs are mostly met with available funds. The funds needed for new investments to meet EU obligations are more or less available from EU and government sources. Funds for reconstruction and rehabilitation of existing assets are declining, and their level is no longer sufficient. According to the National Water Basin Management Plan, about €1.7 billion should be invested from 2014 to 2027, with 30% going toward water projects and 70% toward funding wastewater investments. This represents around €32/capita/year. (KvVM 2010)

Investments. Most investments are related to fulfilling EU directives obligations. Total investments planned in the water sector for 2007-2013 amounted to €2.7 billion, more than 90% of which was financed by EU funds. In 2014, less than half of this planned investment allocation had been spent, which represented an overall effort of €1.35 billion

(average of around €13/capita/year over the period). Ninety-one percent of these funds were spent on wastewater investments and 9% on drinking water projects (Figure 7). The remaining €1.35 billion is to be spent in the coming years for projects already underway.

Cost Recovery and Affordability

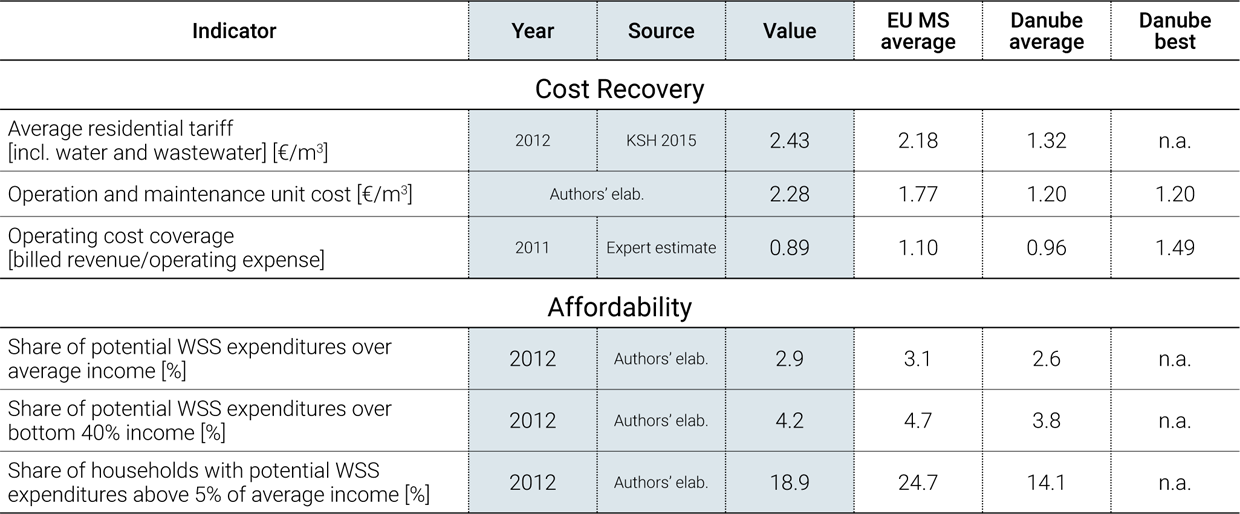

Cost recovery. Operating costs are generally not recovered, and tariffs are not sufficient to fund asset renewal. The Act 209/2011 on water utility services requires full cost recovery in accordance with the Water Framework Directive. However, since the government decree on tariff setting has not been adopted yet, detailed requirements on tariff setting are unknown. Under current practice, operating costs are not recovered, and some utilities need to scale back on specific cost items (such as maintenance), which may be detrimental to long-term service quality. The average operating ratio in the sector is 0.89, but a wide variability is observed among utilities, with ratios ranging from 0.5 to 1.2. Moreover, the indicator value started to decrease by 5% to 10% between 2011 and 2014, due to the government decision to freeze tariffs and then reduce them (Expert estimate). Household tariffs in municipalities facing unit service costs above a threshold value are eligible to receive subsidies from the central government. Such a mechanism does not encourage utilities to improve their efficiency. These subsidies represent about 2% of the overall tariff revenue of the sector.

Electricity purchase

To reach a lower electricity price through higher volume of purchase, some water utilities bundle their electricity purchases from the competitive market. Previously, they acquired electricity individually; now, they enter the market together. A larger total purchase volume is attractive for electricity traders, making it possible to provide lower rates to utilities. Some utilities used auctions to effectively lower the price. Mezőföldvíz Kft., for example, used a decreasing price auction to contract for its 2014 energy needs and achieved a purchase price 10% below the regular market price.

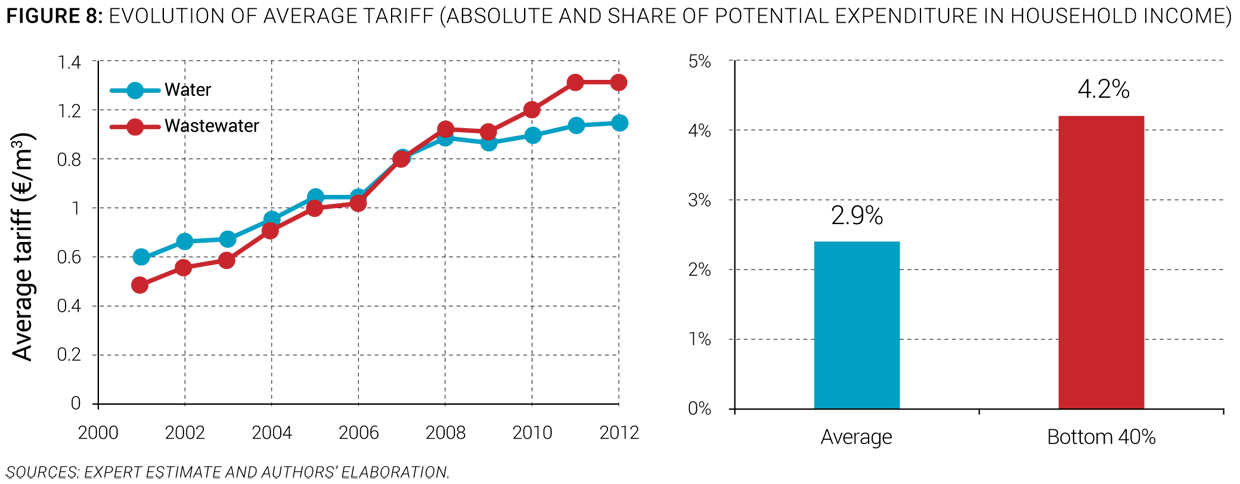

Tariffs. After a substantial increase in real terms during the 1990s and 2000s, water and wastewater tariff evolution followed inflation for the last 7 years. Between 2001 and 2008, water and wastewater tariffs doubled, on average (Figure 8). But between 2008 and 2014, they remained stable following the inflation evolution. Water tariffs paid by commercial entities are higher than household tariffs, since the act on water utility services allows cross-subsidies between users, with the possibility of commercial tariffs being 150% higher than household tariffs.

Affordability. The affordability of water and sanitation is an issue for the low-income population, including marginalized minorities. In 2012, the share of the potential cost of water in the average household budget was close to 3% (Authors’ elaboration). In the bottom 40%, this share amounted to 4.2%, even though their average consumption was only 70% of the average household (Authors’ elaboration). In the poorest 10 subregions (the administrative level below counties), this value reaches 10% (KvVM 2010). Low-income minorities are in a very disadvantaged position, often lacking direct access to piped drinking water.

WATER SECTOR SUSTAINABILITY AND MAIN CHALLENGES

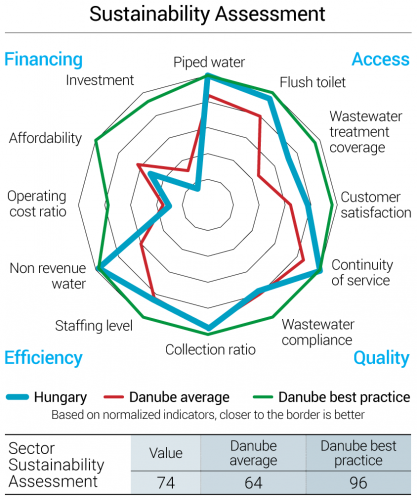

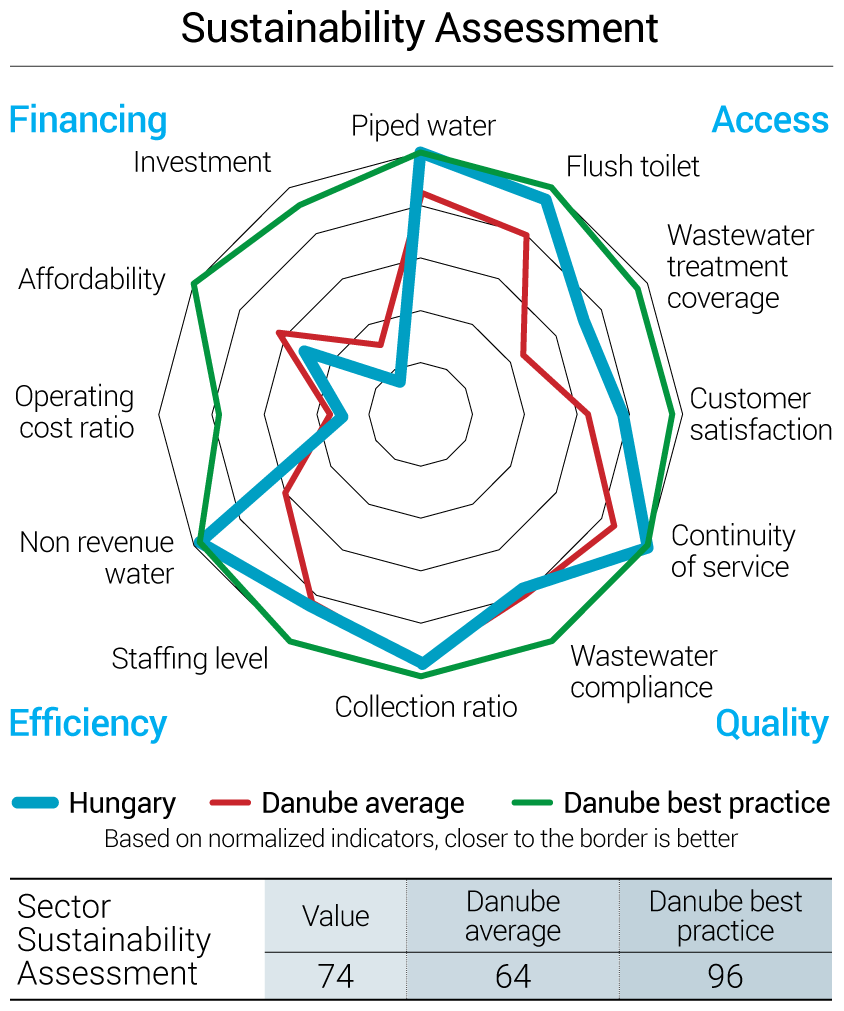

To evaluate and reflect the sustainability of services in the region, an overall sector sustainability assessment was done, taking into account four main dimensions: access to services, quality of services, efficiency of services, and financing of services. Each of these dimensions is measured through three simple and objective indicators. For each indicator, best practice values are established by looking at the best performers in the region, and countries closest to those best performers are deemed to have a more mature sector. A more complete description of the methodology to assess sector sustainability is included in the Annex of the State of the Sector Regional Report from the Danube Water Program. The outcomes of this assessment for Hungary’s water sector are displayed in Figure 9, which also shows average and best practices in the Danube region. The Hungarian sector sustainability score is 74, which is far above the Danube average sustainability of 64, and is among the best practices in the region. The assessment shows that, on average, the country performs well in terms of continuity of access to piped water and flush toilet, collection ratio, nonrevenue water and staffing level. The main deficiencies of Hungary’s water sector identified through the sector sustainability assessment are the operating cost ratio, affordability, and investments (Figure 9)..

The main sector challenges are:

- Achieving full cost recovery. Many of Hungary’s water utilities have carried out EU and government-sponsored investments over the last few years. As a result of the financing agreement, the depreciation of these investments must be covered by tariffs (that is, the part of the tariffs not subject to the tariff freeze and cut), but the costs necessary for maintenance or the additional cost of operation can no longer be added to the tariff base. Thus, a growing inventory of assets needs to be maintained, with shrinking resources for maintenance. Moreover, since water and sewerage tariffs were frozen in 2012, and decreased by law in 2013, revenues collected by utilities are decreasing.

- Preventing the degradation of assets in the longterm. While assets of most water utilities have been properly maintained during the last two decades, few companies made efforts to create sufficient reserves for their future replacement. As a result, the infrastructure is aging and its average condition is slowly declining. The quality of service continues to be good, so the threat of asset decline is not immediate. Due to the 2013 tariff cut, utilities have accumulated even lower reserves than before, and maintenance has become problematic for many operators. Without external support from government grants for investments or an increase in tariff revenues, the trend of asset decline does not seem reversible.

- Preparing for the risks caused by climate change. Most water utility managers are aware of the types of risks caused by climate change (such as new patterns of precipitation, stress on sewerage, changing patterns of water consumption, and change in water resources used for drinking water), but the everyday challenges of maintaining a high level of operation under worsening financial conditions make it difficult to focus on the long term. While the companies have strategic plans, climate change is rarely addressed in them, and risk management systems are usually not in place within the utilities.

SOURCES

- EC. 2014. Synthesis Report on the Quality of Drinking Water in the EU Examining the Member States’ Reports for the Period 2008-2010 under Directive 98/83/EC. Brussels: European Commission.

- Eurostat. 2014. European Commission Directorate-General Eurostat: Statistics Explained - Water Statistics. Accessed 2015. http://ec.europa.eu/eurostat/statistics-explained/index.php/Water_statistics.

- FAO Aquastat. 2015. Food and Agriculture Organization of the United Nations - AQUASTAT Database. Accessed 2015. http://www.fao.org/nr/water/aquastat/data/query/index.html?lang=en.

- Gallup. 2013. World Poll. Accessed 2015. http://www.gallup.com/services/170945/world-poll.aspx.

- Gov. HU. 2015. Hungarian Government. Accessed 2015. http://www.kormany.hu/en.

- GVI. 2013. The Socio-Economic Profiles of the Hungarian Regions. Budapest: Institute for Economic and Enterprise Research.

- IBNet. 2015. The International Benchmarking Network for Water and Sanitation Utilities. Accessed 2015. http://www.ib-net.org.

- ICPDR. 2015. International Commission for the Protection of the Danube River. Accessed 2015. http://www.icpdr.org.

- KSH. 2014. Environmental Report 2013. Budapest: Hungarian Central Statistical Office.

- —. 2015. Hungarian Central Statistical Office. Accessed 2015. http://www.ksh.hu.

- KvVM. 2010. National River Basin Management Plan. Budapest: Hungarian Ministry of Environment and Water.

- TESZIR. 2015. Hungarian Municipal Wastewater Information System. Accessed 2015. http://www.teszir.hu.

- UNDP/GEF DRP. 2004. Assessment and Development of Municipal Water and Wastewater Tariffs and Effluent Charges n the Danube River Basin. Volume 2: Country-Specific Issues and Proposed Tariff and Charge Reforms: Hungary - National Profile. New York City: United Nations Development Programme/Global Environment Facility - Danube Regional Project.

- World Bank. 2015. World Development Indicators. Accessed 2015. http://databank.worldbank.org/data/views/reports/tableview.aspx.